This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

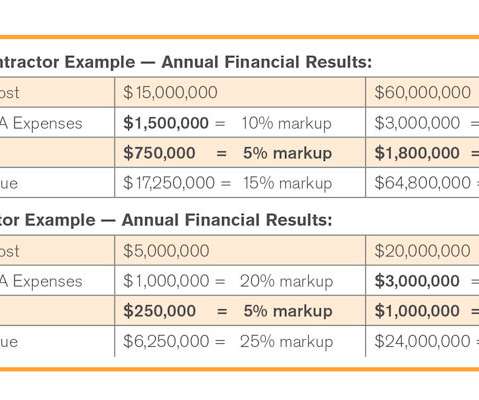

It’s nearly impossible to make any money when contracts allow just 10% and your subcontract only allows for 15% total overhead and profit markup on changeorders, or time and material costs plus work. The typical commercial contractor’s annual overhead and profit markup look much like those in Figure 1.

Colorado Verified Statement of Claims on Public Projects A Colorado Verified Statement of Claim (VSOC) ensures subcontractors and suppliers get paid for labor and/or materials provided to a public construction project. The claim must be signed under oath and only include amounts due for work or materials provided.

One such decision a government contractor might be tempted to make is to accept additional field office (jobsite) overhead (FOOH) expenses for a change on a percentage markup basis, especially for a change that may not even have required an extension to the contract completion date.

This ensures data is always up to date, items like changeorders and RFIs are addressed quickly, and that bills are paid in a timely manner to keep people, materials and work constantly moving. As companies grow, their overhead expenses can also grow.

Some Advice on ChangeOrders » A Change (Order) for the Better? When clients ask me about changeorders, I’m reminded of a well-circulated photo. The yacht is named “ChangeOrder.” Discussion about changeorder difficulties tends to be one of two types.

In this case the "Hammer" is a changeorder. 3% of your customers are "Grinders" and will try to take all your profit by telling you too "Sharpen Your Pencil" which means do the job for just over your hard cost for material and whatever you pay your employees in gross wages with no allowance for overhead costs.

Each task should also have the following break downs and associated information (cost and descriptions as appropriate) for (1) labor, (2) material, (3) construction equipment. Construction supervision, and general office overhead, as well as any other costs should also be itemized separately. via 4bt.us.

project task/line item, a full description in plain English, a unit of measure and a corresponding unit price, including labor, material, and equipment details, and an associated approved contractor coefficient are to be the basis for Contractor compensation. coefficient (reference table of allowable overhead). authorization.

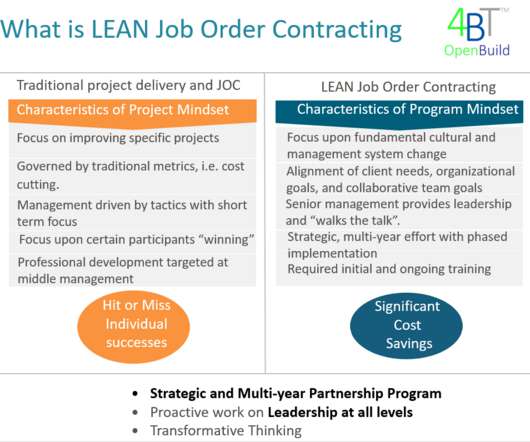

Procurement costs, project delivery times, overall construction costs, changesorders, and legal disputes can all be mitigated via properly established and managed JOC Programs. How Does Job Order Contracting Work? When Is Job Order Contracting Used? Proof That Job Order Contracting Works.

If we’re being honest with ourselves, rework happens on nearly every construction project, whether it’s due to poor craftsmanship, field changes, or errors of omission. It’s fairly easy to determine what rework costs a contractor with regards to labor and material, but determining the true total cost is a whole different beast.

Procurement costs, project delivery times, overall construction costs, changesorders, and legal disputes can all be mitigated via properly established and managed JOC Programs. The UPB should also contain crew information and be updated annually at a minimum, and quarterly if possible for labor and material fluctuations.

Material Cost – Description and cost of materials associated with specified task. Thus costs estimates should first be prepared WITHOUT including OVERHEAD and PROFIT. It’s no surprise to anyone that errors and omissions are largely the cause of cost creep, changeorders, and general dissatisfaction.

Adversarial, change-order-oriented environment is common between owner, A/E, and contractor. Bid shopping can occur and actual overhead and profit amounts are unknown. Changeorders may be reduced versus DBB due to A/E-contractor collaboration and contractual relationship. Disadvantages. Owner has less control (vs.

Labor for each construction task described in a line item is based upon local prevailing wages (or Davis-Bacon Wage Rates as determined by the contract/client), materials, and equipment rates, associated crews, and productivity. If a UPB is properly created it consists of “bare costs” only (no contractor overhead or profit).

Material Cost – Description and cost of materials associated with specified task. Thus costs estimates should first be prepared WITHOUT including OVERHEAD and PROFIT. It’s no surprise to anyone that errors and omissions are largely the cause of cost creep, changeorders, and general dissatisfaction.

There are three general elements to an estimate: 1) the direct cost of the installed materials, including labor; 2) indirect, or support costs, such as scaffolding, crane usage, testing, inspection and punch lists; and 3) markups, such as overhead, profit and contingency, or risks.

Material Cost – Description and cost of materials associated with specified task. Thus costs estimates should be prepared WITHOUT OVERHEAD and PROFIT. It’s no surprise to anyone that errors and omissions are largely the cause of cost creep, changeorders, and general dissatisfaction.

Construction Forms for Excel include : Estimation Forms for Construction: Bid Plan Log, Time and Materials Log, Estimate Sheet, Job Estimate, Telephone Bid Sheet, Itemized Proposal, Job Cost Report, Take Off Estimate, Time and Materials Estimate, Request for Proposal Log, Overhead Calculation.

fraught with rising costs, material challenges, and labor struggles—the pressure to answer these questions correctly becomes even greater. of construction materials in the RSMeans database experienced a significant cost increase, with an average increase of 19%. EC3 is a free tool that helps users choose carbon-smart materials.

This construction estimating book contains an extensive database of electrical costs and electrical materials which are based RS Means Database. With this book the electrical contractors will be able to provide the total cost for materials, labor , overhead and profit precisely.

National Construction Estimator contains the following features :- • Modify any price or quantity related to any construction material in the construction estimate window. Arrange your own labor rates, overhead and profit. • Put in your genuine construction material costs.

Instead of operating from a fixed location with a fixed set of products or services, construction projects rely on a range of locations, materials, and services. To make things even more complex, items that you might consider overhead expenses are often actually costs of goods sold because they are connected to a client project.

Tracking changeorders in QuickBooks for Contractors for each job. Double checking to make sure the contractor gets paid for all changeorders. Enter purchases of material, supplies, equipment rental, tools and other items. Separate direct and indirect job costs from overhead. Organize loose materials.

His price will typically be set to cover overhead costs and a reasonable profit. If quality is an owner’s priority, some think that “cost-plus-a-fee” contracts – reimbursement for labor and materials expenses, plus either a percentage or a fixed amount for overhead and profit – are the way to go.

Bigger projects require more materials and more labor, which means higher cash requirements. And in construction, you can’t bill for the work until you’ve completed it — which means there’s an even longer delay from when you purchase materials or provide the work and get paid. Finance material purchases. Poor planning.

Sometimes this unanticipated time/space compression is the owner’s fault, in which case the general contractor/construction manager and its subcontractors will likely be entitled to increased compensation by changeorder or otherwise -- and to a mechanic’s lien if that increase is not paid. But how is that sum calculated?

Standardized, Common Information for Costs, Materials, Equipment, Processes (i.e. Average project timeline. %/#/$ Changeorders. are: shorter procurement times, fewer changeorders, virtual elimination of legal disputes, and more projects completed on-time and on-budget. Early and Ongoing Communication.

Construction estimating involves the estimating of material, labor, equipment, overhead/profit and contingencies. White Paper – Cost Estimating Evolution .

In the construction industry, WIPs cover the raw materials, plus labor and overhead, used as part of a project. Meaning, they’ve likely paid for most of the materials, labor, and overhead a while back. This might mean they haven’t sent an invoice or, it could mean that changeorders have not been approved.

That is when Mom would launch the opening salvo as she tried to explain why all of the materials and other related job costs that had been purchased were used on a variety of job sites. ChangeOrder. Overhead & Profit Charges. When my parents used words like: Job Deposit. Payment Application. Periodic Draw.

The contract includes a unit price book (UPB) that establishes a unit price to be paid for each of a multitude of construction line items including pre-priced/pre-negotiated items of work and materials. Advantages typically associated with JOC – Job Order Contracting Programs: Fast and timely delivery of projects. – INCOM 2009.

Advantages of Job Order Contracting – JOC – for OWNERS. fewer changeorders, increased response to warranty issues, virtually no legal disputes. Advantages of Job Order Contracting – JOC – for CONTRACTOR. improved quality of project delivery and end results. overall project time savings.

Sage Estimating also facilitates forecasting the labor, raw material and other overhead costs so that the contractors can arrange & deliver correct bids. As soon as the project is procured, estimate details flow automatically into Sage business management software, removing unnecessary tasks and data entry errors.

In the construction industry, WIPs cover the raw materials, plus labor and overhead, used as part of a project. Meaning, they’ve likely paid for most of the materials, labor, and overhead a while back. This might mean they haven’t sent an invoice or, it could mean that changeorders have not been approved.

Provided labor and material for somebody''s home or business without a deposit check. Did changeorder work that you never got paid for doing and never will. Just like house builders love chatting with sub-contractors and building material suppliers because you all speak the same language.

The coefficient must include not only the contractor’s overhead and profit, but also any adjustment that may be needed to the UPB prices based on the contractor’s costs in the local area of the contract(which are functions of labor costs, subcontractor base, market conditions and client-specific conditions).

Differences in GHG in alternatives resulted from the amount of new building materials introduced and transportation of demolition debris. Cost estimates and construction bid requests should include materials quantities in addition to costs to evaluate and validate GHG impacts. Recommendations.

JOC, an annual contract and multiple option year agreement for general construction, generally requires the Contractor to e furnish associated labor, tools, materials, equipment and transportation. Job Orders / Task Orders. All cash discounts should be deducted in determining material costs.

Differences in GHG in alternatives resulted from the amount of new building materials introduced and transportation of demolition debris. Cost estimates and construction bid requests should include materials quantities in addition to costs to evaluate and validate GHG impacts. Recommendations.

o Determine costs/pricing structure (labor, materials, overhead, etc.). Demonstrate knowledge of fall protection of people and tools/materials for contractor and occupants. Demonstrate knowledge of proper disposal of hazardous, toxic and biologic materials. operability with accounting system. o Establish close-?out

We organize all of the trending information in your field so you don't have to. Join 116,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content