This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

Inside Construction's 2024 Risk & Insurance Landscape ccapoccia Mon, 04/01/2024 - 17:00 Uncertainty has defined the construction landscape for several years now. That change can alter your business’s risk — and the insurance necessary to protect it. That change can alter your business’s risk — and the insurance necessary to protect it.

Proactively Tailoring Your Insurance Plan to Intercept Future Risk. When there are disruptions, from factors such as staffing issues, resource allocation, supply chain delays or downtime from damaged equipment, economic havoc can erupt. Tue, 06/14/2022 - 13:49. Construction projects run on a strict timetable.

Having snow removal insurance is important, considering the risks and dangers of snow removal and deicing. This article will show you the things you need to know about snow removal insurance. . What Is Snow Removal Insurance? Snow removal insurance can offer a wide variety of policies to protect contractors and their businesses.

For those installing properties using rigging equipment, the complexities of these job sites are even worse. Fortunately, crane and rigging insurance provide protection and compensation. However, understanding these insurance policies is key to maximizing your benefits. What is crane and rigging insurance?

The cost of theft in the construction industry is estimated to be a billion dollars by the National Insurance Crime Bureau. Unsecured equipment and materials are especially at risk. Additionally, heavy equipment owners can’t rely entirely on insurance to offset the cost of theft. Equipment Keys.'

Either by choice or required by contract or statute, commercial general liability (CGL), workers’ compensation, business auto and inland marine insurance (mobile equipment) are among the most common types of insurance purchased by contractors.

11, 2012) – The American Rental Association (ARA), ARA Insurance and the National Equipment Register (NER) has named Detective Terry Haldeman of the Snohomish County Auto Theft (SNOCAT) Task Force in Everett, Wash., as the winner of the ARA Insurance/NER Theft Award for 2012. MOLINE, Ill.

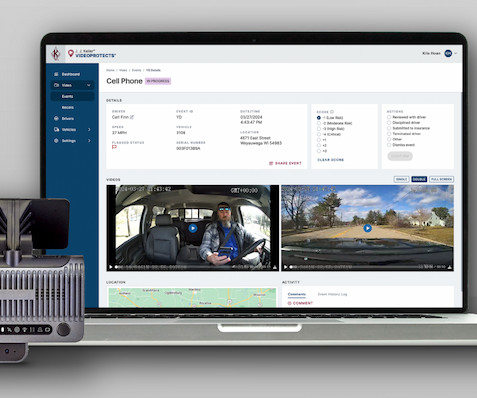

Yet, even as equipment has become safer, highway fatalities are increasing at an alarming rate, and insurance companies have targeted distracted driving from cell phone use as a contributing factor.

Between the potential for accidents and injuries on the job site and the risk of lawsuits, it’s important to have insurance to protect yourself from financial losses, but what kind of insurance do you need? Here’s an overview of the most important types of insurance for contractors. General Liability Insurance.

Capturing accurate equipment information is a challenge that many contractors face. Data collection and analysis has traditionally been a manual process, and many times information would slip through the cracks leading to equipment being poorly maintained, overused or even retired before necessary.

Burrows Professor Emeritus of Construction Engineering at Virginia Tech and is author of Construction Equipment Economics , a handbook on the management of construction equipment fleets. His ideas and methods regarding the management of heavy equipment are, in my opinion, the gospel for the industry. Owning Rates.

Equipment. General insurances. Workmen’s compensations insurance. Workmen’s compensations insurance. State unemployment insurance. Federal unemployment insurance. Incidental tools and equipment. Labor (Both during Normal Work Hours and Outside of Normal Work Hours). Materials. Supervision.

Operators who know how to properly and safely use their equipment are not only much more likely to operate it safely, but they also are able to work faster and more efficiently, leading to better overall performance. Performance leads to profits, and fewer accidents result in fewer expenses and insurance claims.'

If you, as an employer, have 1099 employees on your staff from time to time, you may be wondering whether you are required to provide health insurance to them. Though, they usually don’t get the same benefits as full-time employees, and must provide their own equipment for jobs. What is a 1099 Employee?

Insurance companies offer usage-based insurance (UBI) in the automotive industry, but heavy equipment managers will probably not find anything similar for several years. UBI uses telematics to tie insurance costs to the way a vehicle is operated. Equipment managers may still benefit from telematics…

According to the National Insurance Crime Bureau, as much as $1 billion in construction tools, equipment and materials is stolen nationwide each year, 90 percent of which is taken directly from construction sites. Throughout the last decade, the construction industry has spawned an entirely new black market industry—construction theft.

There are all sorts of equipment and materials needed to start a roofing and guttering business. Roofing equipment and materials. Insurance, liability, and workers’ compensation . 3) Equipment and materials. Roofing and guttering equipment and materials need to be acquired before you can start your business.

The goal is to identify and address dangerous behaviors before an accident happens, protecting your company’s equipment from damage … your employees and others on the road from harm … your company from costly litigation … your insurance rates from skyrocketing … and your brand name from bad publicity. In a recent J.

Improved asset lifespan: Proactive maintenance strategies based on TCO analysis can extend the life of equipment and reduce unexpected breakdowns. Consider energy efficiency upgrades: Evaluate opportunities to reduce energy consumption through building retrofits and equipment upgrades.

Zurich North America offers Construction Weather Parametric Insurance does not require physical loss or damage in order to claim weather-related losses. Parametric insurance sets predetermined parameters and payments—agreed upon by the insurer and the customer during the application process—for…

Business insurance can help mitigate occurrences or disasters that can severely impact or destroy the good standing of your business. Let’s take a look a subcontractor insurance: when it’s needed, what happens if a sub goes uninsured, and what policies subs can use to protect their businesses from risk.

One way to help protect yourself from some of these perils is by having business interruption insurance for construction. This type of insurance can help ensure that you’re able to continue operations if something happens that causes you to lose income. What does business interruption insurance cover ?

Burrows Professor Emeritus of Construction Engineering at Virginia Tech and is author of Construction Equipment Economics , a handbook on the management of construction equipment fleets. His ideas and methods regarding the management of heavy equipment are, in my opinion, the gospel for the industry. Owning Rates.

In today’s ever-evolving insurance landscape, the importance of swift and efficient claim resolution cannot be overstated. Let’s embark on a thorough exploration of how Contractor Connection partners with the insurance industry, delivering a holistic, efficient, and dependable claim journey.

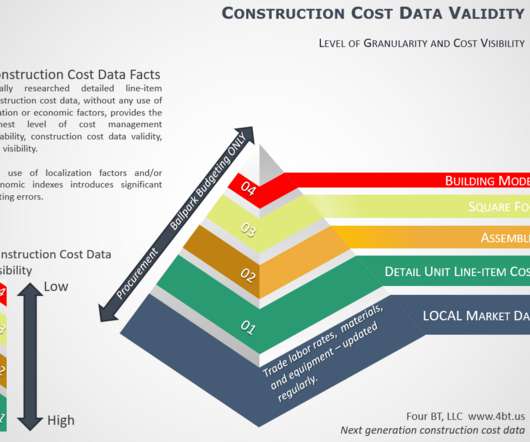

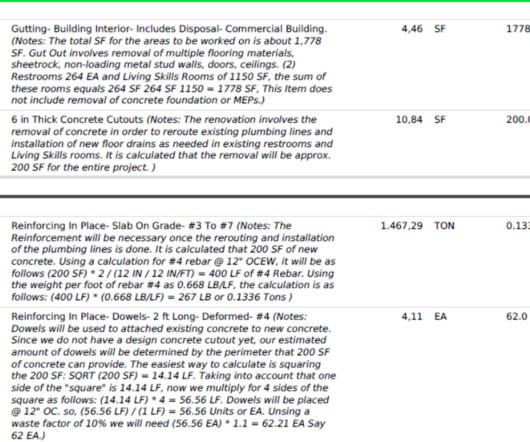

An actionable unit price cost database includes granular repair, renovation, maintenance, and new construction tasks for the local market and includes labor, material, equipment, crew, and productivity information, per an associated unit of measure. for the local market. Profit and overheads should be considered separately.

Are you ready to equip your construction site with top-tier security solutions? Regarding your tools and equipment, you must be vigilant about who checks each item. You can implement RFID tracking to make the equipment logging process more accurate and efficient.

Help with negotiations This can be difficult, as insurance companies are often reluctant to pay large settlements. An experienced attorney will know how to negotiate with insurance companies and fight for the best possible settlement for you. Contributory negligence This defense says that you were partially to blame for your injuries.

With the amount of money you invest in tools and equipment, it’s crucial to protect those assets no matter where you go. Your base insurance policy may offer some coverage for unexpected damage to some business property, but making assumptions about the extent of coverage could lead to some financial distress. .

liability insurance and allowance for small tools and consumables. Liability insurance based upon local contractor rates is also added as a percentage. Equipment Costs. Equipment costs are either local rates or a national rate for each piece of equipment used in crews performing the task based upon daily usage.

Employers should not assume that workers provided by those staffing companies have been adequately trained in safety, especially since “OSHA requires that forklift certification be site and equipment specific. 2) Ensure operators are certified for your site and your forklift equipment and are completely competent to operate it.

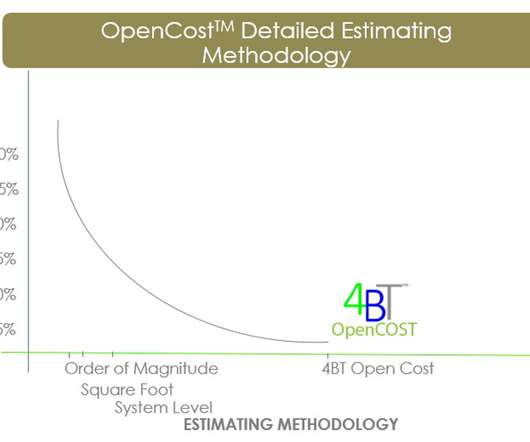

. #3 Building a Detailed Estimate The best approach to completing is to create a detailed line item estimate via a quantity take-off and associating granular labor, material, equipment, and productivigy data for each line. This will provide you with a clear technical and cost view of the project. #4

Well, now at least one insurance company believes that, as well. I’ve admittedly been focused mainly on the productivity gains from using technology, but getting a discount from an insurance company to use it is an interesting side effect. Announced today, The Travelers Companies, Inc.

For example, if you completely own a piece of equipment, you probably estimate the amount of fuel that it uses on a job, but may not consider including the depreciation, insurance, maintenance, and other costs associated with running it. All of these expenses are important to include for your bid to be accurate.

An important principle governing the use of personal protective equipment was reaffirmed recently in a Washington state case involving a bank guard who was stabbed and was not wearing body armor. The company appealed and the matter was heard by a hearing officer for the state Board of Industrial Insurance Appeals.

INSURANCE |. EQUIPMENT |. Equipment Management. Equipment and Services Directory. Most of these contractors are considering an investment in equipment or software, and they want to know if it can actually help their construction business. Good on new and used equipment, including software. SOFTWARE |.

Let’s say a subcontractor’s insurance has expired. With the right integrated software system, you are alerted if the insurance is not up-to-date. Then you can hold payments until the insurance issues are cleared up. Another risk common to construction companies is the chance of equipment damage.

The president/CEO of American Rental Association Insurance will retire at the end of February. Kelling has been with ARA Insurance since 1997, and led ARA Insurance to grow from a small insurance agency with four independent agents to… Phil Kelling will be replaced by John Kennedy, the current CFO.

These include soft costs – general conditions, insurance/bonding, fees/permits, as well as direct costs for material, equipment, and labor in elemental CSI MasterFormat data architecture.

Whether you’re just starting your business or looking to change insurance carriers, it pays to go with a company that has experience and knowledge in providing insurance for the construction industry. These days you can purchase insurance on your own or go through a local agent. Best construction insurance companies.

These include expenses like payroll taxes, benefits, insurance, and other indirect costs understanding labor burden. Benefits : Health insurance, retirement contributions, and other employee benefits add to the labor burden calculating benefits costs. What is Burden Rate in Construction?

Luckily, that’s what insurance is for, right? Does a general contractor’s insurance cover their subcontractors’ accidents or mistakes? While there isn’t a cut-and-dry answer to these questions, we’ll take a deeper look into insurance coverage and what happens in these situations. Who is covered by an insurance policy?

We organize all of the trending information in your field so you don't have to. Join 116,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content