This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

Inside Construction's 2024 Risk & Insurance Landscape ccapoccia Mon, 04/01/2024 - 17:00 Uncertainty has defined the construction landscape for several years now. That change can alter your business’s risk — and the insurance necessary to protect it. That change can alter your business’s risk — and the insurance necessary to protect it.

The cost of theft in the construction industry is estimated to be a billion dollars by the National Insurance Crime Bureau. Unsecured equipment and materials are especially at risk. Additionally, heavy equipment owners can’t rely entirely on insurance to offset the cost of theft. Equipment Keys.'

Your leadership team spends hundreds of hours agonizing over any one project's schedule—what workers should be hired for which phase of the project; what materials should be shipped to the site when; when and how often project owners should be brought in for a status update; and more.

These costs have surged due to a combination of factors, including supply chain disruptions, labor shortages, increased material prices, and evolving regional risk exposures. However, in the face of rising costs and shifting risk landscapes, these insurance options are becoming increasingly complex to navigate.

Between the potential for accidents and injuries on the job site and the risk of lawsuits, it’s important to have insurance to protect yourself from financial losses, but what kind of insurance do you need? Here’s an overview of the most important types of insurance for contractors. General Liability Insurance.

Materials. General insurances. Workmen’s compensations insurance. Workmen’s compensations insurance. State unemployment insurance. Federal unemployment insurance. Shipping of all materials to the jobsite. Labor (Both during Normal Work Hours and Outside of Normal Work Hours). Equipment.

There are all sorts of equipment and materials needed to start a roofing and guttering business. You’ll also require the following: Vehicle that can handle transport of materials. Roofing equipment and materials. Roofing equipment and materials. Insurance, liability, and workers’ compensation .

Common expenses for operating a construction business include labor, materials, insurance, permits, office space, vehicles, trailers and other incidentals. Despite its simple appearance, the financial equation of “revenue - expenses = profit” is so complex, there are few who truly understand it.

According to the National Insurance Crime Bureau, as much as $1 billion in construction tools, equipment and materials is stolen nationwide each year, 90 percent of which is taken directly from construction sites. Throughout the last decade, the construction industry has spawned an entirely new black market industry—construction theft.

liability insurance and allowance for small tools and consumables. Material costs are either. Liability insurance based upon local contractor rates is also added as a percentage. Material Costs. Material costs are local for commodities such as concrete, asphalt and aggregate. Quality / Quantity.

Even though the insurance company isn’t your customer, the property owner may be depending on that insurance check to pay for your work. Meanwhile, you’re incurring expenses that drain your bank account, like purchasing materials and paying employees. Restoration contractors can spend a lot of time waiting for payment.

FEMA Moves to Improve Flood Insurance Program. NAHB Policy Brief | The next phase of the National Flood Insurance Program is supposed to better reflect the actual risks to properties; builder confidence increased during April. . As a result, some insurance rates will go up while others will go down. Mon, 05/10/2021 - 06:00.

As a contractor, you rely on the property owner to pay you for your work and materials. In turn, the owner is relying on the insurance company to pay their claim. After all, the faster the insurance company pays the owner, the quicker you can get paid ! You may feel the urge to step in and help with the adjuster.

Your leadership team spends hundreds of hours agonizing over any one project's schedule—what workers should be hired for which phase of the project; what materials should be shipped to the site when; when and how often project owners should be brought in for a status update; and more.

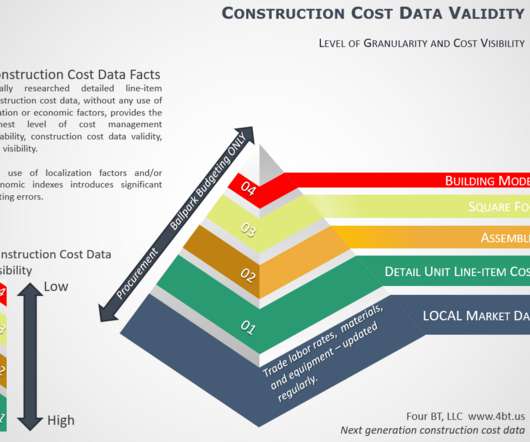

An actionable unit price cost database includes granular repair, renovation, maintenance, and new construction tasks for the local market and includes labor, material, equipment, crew, and productivity information, per an associated unit of measure. for the local market. Profit and overheads should be considered separately.

mhodges Mon, 12/04/2023 - 08:13 According to Joe Tejeda, Practice Leader for PCF Construction, one of the most pressing issues in the construction industry today is the unforeseen or unintended increase in risk exposures due to rising construction material costs.

Water damage resulting from inefficient or ineffective water management on jobsites causes significant losses for contractors resulting from delays, material costs, remediation and removal, reputational damage or skyrocketing insurance premiums.

HM Revenue & Customs is turning the spotlight on claims for rising materials costs under the industry’s CIS tax scheme. It’s quite apparent that this is part of a targeted campaign aimed at challenging the materials cost element included in invoices submitted by subcontractors for services provided to contractors. “A

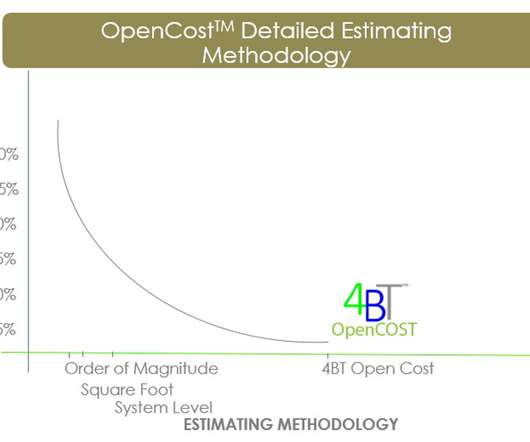

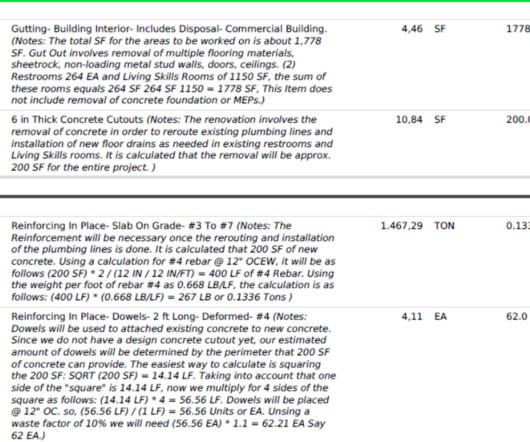

3 Building a Detailed Estimate The best approach to completing is to create a detailed line item estimate via a quantity take-off and associating granular labor, material, equipment, and productivigy data for each line. This will provide you with a clear technical and cost view of the project. #4 expanded CSI Masterformat ). #5

For example, if you completely own a piece of equipment, you probably estimate the amount of fuel that it uses on a job, but may not consider including the depreciation, insurance, maintenance, and other costs associated with running it. All of these expenses are important to include for your bid to be accurate.

It covers land acquisition costs, building materials, construction permits, labor, contingency and interest reserves, closing costs, and plans. Find out if you can use your land equity towards your down payment, how they pay construction draws, and if the contractor can request a draw to cover material costs.

Construction companies constantly seek insurance solutions that can provide material financial impact, limit their contractual exposures and provide coverage enhancements. The following are four strategic solutions which can provide substantial financial protection for construction companies.

Construction companies constantly seek insurance solutions that can provide material financial impact, limit their contractual exposures and provide coverage enhancements. The following are four strategic solutions which can provide substantial financial protection for construction companies.

These include soft costs – general conditions, insurance/bonding, fees/permits, as well as direct costs for material, equipment, and labor in elemental CSI MasterFormat data architecture.

Managing Rising Construction Costs: Insurance. Builders and remodelers may be subjected to coinsurance penalties as a result of rising building material prices if they do not make changes to their policies. If the insured fails to maintain the coverage, possibly due to changing costs and values, the insured is subject to a penalty.

Navigating the insurance requirements for construction projects can be daunting. Insurance plays a crucial role in managing risks and ensuring the successful completion of any construction project. For more details on CGL insurance, visit Construction Coverage. Explore Stonemark’s insights on project-specific insurance.

Project loss insurance has the potential to save contractors from devastating project losses, no matter the cause. Project loss insurance, or PLI, is designed to mitigate catastrophic construction project losses. Project loss insurance coverage. How project loss insurance works. How much does project loss insurance cost?

Luckily, that’s what insurance is for, right? Does a general contractor’s insurance cover their subcontractors’ accidents or mistakes? While there isn’t a cut-and-dry answer to these questions, we’ll take a deeper look into insurance coverage and what happens in these situations. Who is covered by an insurance policy?

Plumbing contractors should include business insurance as an integral part of their financial strategy. With numerous policies available, the plumbing contractor’s insurance landscape offers many ways for you to protect your physical and financial business assets. What is plumber’s insurance? Worker injury.

Insurance is one part of a strategy to keep your carpentry business financially healthy. To minimize any financial damage, a comprehensive carpenter’s insurance plan is a smart bet. . What is carpenter insurance? Does a carpenter need insurance? Insurance serves another purpose.

As Florida markets work to rebuild from devastating Hurricane Ian, homeowners are confronted with inflated prices for building materials, adding insult to injury amid comprehensive recovery efforts across the Sunshine State. Building material prices fell 0.3% Building Materials. Building Materials.

When working in construction, your insurance policy gets issued as a fairly standard contract. Like a basic construction agreement, you can upgrade or downgrade your insurance policy just as a customer might do with the fit and finish of a building. What is an insurance endorsement? How insurance endorsements work.

Your base insurance policy may offer some coverage for unexpected damage to some business property, but making assumptions about the extent of coverage could lead to some financial distress. . An equipment floater offers insurance protection for your business property as it moves from location to location. What is an equipment floater?

Consider project delays, legal battles, insurance rate increases, and the damage done to your companys reputation. Lower Costs and Fines The up-front cost of safety training pales in comparison to the cost of OSHA violations, legal fees, and skyrocketing insurance premiums. Think about it as paying for peace of mind.

Construction insurance can be confusing. Each contractor and party to the project has their own insurance, which may or may not be adequate to protect the work they’re performing. Learn more: What types of insurance do contractors need? Learn more: What types of insurance do contractors need? CCIP vs. OCIP insurance.

As we planned to provide immediate assistance to our clients in Florida, we were sure to plan for resources unlikely to be available in the aftermath of a storm – namely, electricity, construction materials and manpower.

Check out several tips to ensure a successful roof installation below: 1) Choose The Right Material. If you want a successful roof installation, a significant consideration to think about is the roofing material. When choosing the right materials, some essential factors to keep in mind are its price, appearance, and lifespan. .

We know many of you have had a busy summer, so it’s a good time to take a breath and see what’s been going on in our industry (like rising material costs), as well as what’s on the horizon (like more green building ). The prices of construction materials like metals, asphalt and gypsum have increased since last year.

Employee payroll taxes, insurance, and fringe benefits. All waste and excess material. Sales tax on material and equipment costs. Subcontractors’ overhead and profit. All costs associated with bonding (specifically including bond premiums). Clean up.

Less than 25% of stolen construction materials are returned to the company. It is known for construction site staff to steal equipment while on the job, which is why keeping detailed logs of who has each item can help you to spot and protect yourself against potential theft, which you might need to make an insurance claim for down the line.

It costs a lot to buy the materials you need, and you’ll have to hire a licensed professional to come and do the work. It’s also best to work with a licensed and insured plumber so that the work is guaranteed high-quality and safe. That’s nice, especially if you’re on a tight budget or running low on cash. .

As prices for building materials continue to rise, so too does the incentive for thieves overtaking construction sites. The scarcity of in-demand building materials like copper, aluminum, and lumber has led to significant price gains, and thieves are taking note, says Deseret News. Building Materials. Building Materials.

Example include, general and administrative and other overhead costs, insurance costs, bonding and alternative payment protection costs, protective clothing, equipment rental, and contractor’s profit. Employee payroll taxes, insurance and fringe benefits. All waste and excess material. Sales tax on material and equipment costs.

Consider Insurance and License. Besides that, if they are insured, you can be sure they will not become a liability in case they suffer an injury in the process of doing their job. Besides that, if they are insured, you can be sure they will not become a liability in case they suffer an injury in the process of doing their job.

We organize all of the trending information in your field so you don't have to. Join 116,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content