This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

For small business owners like you, understanding this process could be the key to increasing your profitability and ensuring that every job is priced right. Welcome to a world where every material, labor, and overhead cost is meticulously tracked to unveil the actual cost of doing business.

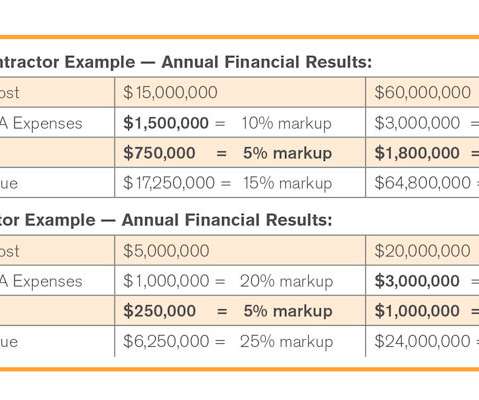

It’s nearly impossible to make any money when contracts allow just 10% and your subcontract only allows for 15% total overhead and profit markup on change orders, or time and material costs plus work. The typical commercial contractor’s annual overhead and profit markup look much like those in Figure 1.

People and material make up the lion’s share of a contractor’s overhead, so it’s no surprise that efficiently managing these is the best way for contractors to improve their profitability. 5 Technologies the Modern GC Should Be Using in 2021. Alex Headley. Fri, 05/28/2021 - 07:30.

After calculating material quantities with your takeoff, estimating adds costs to all facets of the project, from materials and labor to overhead and markup. Waste and overhead can also be added to arrive at the project cost. A unit cost estimate uses the measurements from each takeoff.

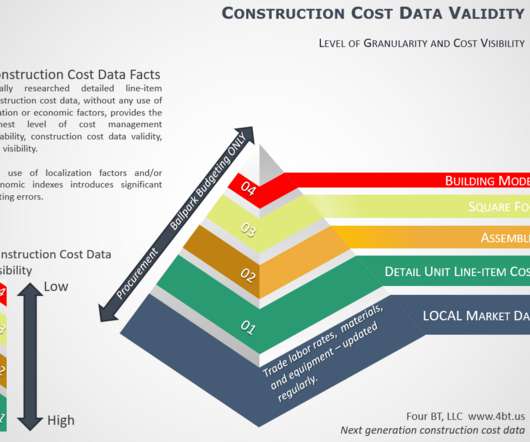

A fundamental element is Job Order Contracting (JOC) is line item estimating which involves breaking down the cost of construction into discrete, granular tasks, each item representing a specific material, labor, and equipment components. Each aspect, such as materials, labor, equipment, and overhead, should be itemized separately.

Understanding COGS isn't just about accountingit's about making smart decisions for profitability, pricing, and more. These include materials, labor hours, and even manufacturing overheads. COGS provides critical insights into your business's efficiency and profitability. What is the Cost of Goods Sold (COGS)?

It should be used to account for contractor overhead and profit. It should NOT BE USED to account for fluctuations in material costs, labor rates, and other factors that can change during the contract term. ( should simply include contractor overhead and profit. Cost Adjustment : A coefficient less than 1.0

Materials. General / Prime Contractor Overhead. General / Prime Contractor Profit and risk. Shipping of all materials to the jobsite. Items included in a JOC coefficient (also known as a “Bid Factor”). Labor (Both during Normal Work Hours and Outside of Normal Work Hours). Equipment. Subcontractor costs.

Material costs are either. The base rate does not include overhead and profit, however, can be added if needed. Material Costs. Material costs are local for commodities such as concrete, asphalt and aggregate. Material costs are local for commodities such as concrete, asphalt and aggregate.

An actionable unit price cost database includes granular repair, renovation, maintenance, and new construction tasks for the local market and includes labor, material, equipment, crew, and productivity information, per an associated unit of measure. Profit and overheads should be considered separately. for the local market.

The coefficient generally must include all project general conditions as described in the contract, including but not limited to supervision, overhead and profit. Updating labor on a more frequent basis and adjusting materials based upon major shifts should also be considered. For instance, a coefficient of 1.20

Maybe you started your company with a few friends and relatives as your earliest clients, and you thought your overhead expenses would be low since you worked out of your home. You made a decent living for yourself, hired a few sub-contractors per project, paid your suppliers, and earned a profit—at least that is what your tax preparer said.

Comprehensive, granular, line item tasks including a description, and individual data components for labor, material, equipment, and productivity (crews). No inclusion of builder/contractor overhead or profit. Organization using expaned CSI Masterformat. Timely updates – Data must be update quaterly at minimum.

Here’s a listing of what is typically included in a construction contractor’s Job Order Contract coefficient… Contractor’s overhead and profit. Subcontractors’ overhead and profit. All waste and excess material. Sales tax on material and equipment costs.

The disconnect between these entities has created problems in the past, and focusing on these connections enhances collaboration and improves the profitability of construction projects. “ As companies grow, their overhead expenses can also grow.

Example include, general and administrative and other overhead costs, insurance costs, bonding and alternative payment protection costs, protective clothing, equipment rental, and contractor’s profit. Subcontractors’ overhead and profit. All waste and excess material.

For example, crews in the field can benefit from analysis that predicts material ordering needs, ensuring that the right materials are always on hand when they need them while project managers can streamline project planning by having material orders built into workflows. Streamlining, Simplifying Construction Data.

home office overhead; insurance, bonds, and indemnification; project meetings, training, management and supervision; mobilization and close-out for the contract and each Project/Job Order; project office staff and equipment; profit; subcontractor’s overhead and profit; all taxes for which a waiver is not available including material sales tax (..)

Answer: A unit price is a detailed description and associated material, labor, and equipment line item within a Job Order Contract Unit Price Book, UPB. When used in Job Order Contracts, a unit price historically does not include contractor profit and overhead as this is account within the JOC co-efficient. What is a unit price?

Each line item represents a discrete individual renovation, repair, or new construction task which includes a description, a unit of measure, crew information, and associated labor, material, and equipment, detailed costs in addition to a total cost. For example, using location factors can result in 30%+ error in labor costs alone.

Overlooking such demands can lead to a loss of market share, a bad reputation, and low profits. Therefore, in 2023, manufacturers will have to contend with longer lead times, high overheads, and poor product quality; all these can negatively impact manufacturing timetables, consumer fulfillment, and profits.

Cost of Material 13. Addition for Overhead and Profit 14. The Construction Estimating Conundrum. Line Item Estimating Details. Choice of work Method. Output of crew. Cost of labor 13. Construction Estimator Skill Requirements for Detailed Unit Price Line Item Estimating. Variability of Estimates. Accurate Estimate – An Oxymoron.

Coefficient make up defined in contract and examples of items that may be including are overhead, profits, taxes, fringe benefits, permits, clean up. (Specifically for Job Order Contracting, though Integrated Project Delivery is similar and used for major new construction). Owner competency and leadership.

Reviewing QuickBooks Profit And Loss Reports - From our construction accounting clients reminded me of something I learned in my own construction businesses a long time ago. Change is not always easy but it’s necessary to grow a healthy and profitable construction business.

Knowing which contract to use when is critical to ensuring a successful outcome in delivery, customer satisfaction, and profit. Knowing which general construction contract to use and when to use one is vital to a successful project, your customers’ satisfaction, and your profits. time and materials contract. Key Takeaways.

The UPB is a set of line item unit costs including detailed a description of the task(s) and associated material, labor, and equipment breakdowns. Contractor applies a coefficient to project / task order costs calculated using the UPB – Coefficient incorporates overhead, profit, and other potential variables.

First, there are several levels of estimate ranging from conceptual to detailed line item, including quantities, equipment, material, and labor costs. Second, there is the estimating process and associated source materials. Contractor Overhead & Profit. Quantities.

Construction Profits Are Simply. Income - COGS - Expenses] = Profit. "If Let''s Get Some Answers - Contractors and sub-contractors know there is more to profits than what is shown above and most of you rely on your "gut feel" to know when project has made a profit or not. With Bonus Material On Cash Flow.

Bare costs (no contractor overhead and profit). The latter are accounted for by the job order contractor’s coefficient(s) as approved for the related Job Order Contract.

It is a listing of construction tasks, organized using MasterFormat, including a detailed line item description and unit pricing for labor, material, and equipment. It is critical, however, that the tasks and the prices reflect labor, material, and equipment specific to the area in which the JOC is located.

Each line item in the UPB should represent a repair, renovation, or construction related task and include… organization via CSI MASTERFORMAT, a title and description in plain English, and detailed subcosts for labor, material, and equipment. that reflects contractor overhead and profit, and other items as allowed via the contract.

This practice does not work for material, labor, equipment, nor does it account for local market productivity in any effective manner. Locally researched JOC Price Books are readily available to provide cost visibility, cost transparency, and therefore improve cost management.

Preliminary costs in construction impact your entire project, and you’ll find that they cover a broad range of equipment, labour, and materials. With more contracts becoming collaborative , contractors are taking on more and more design work to put their material and methods expertise to use. Mockup, testing, and sampling costs.

Material costs and labor hourly rates increased by 2 percent in 2014, and as of now are predicted to continue to grow at that rate per year. Contractor’s overhead and profit margins remained competitive, but are showing signs that they will increase in 2015. Since the start of 2014 the market has been steady but fragile.

Hard Construction Costs are the detailed tasks, materials, equipment, and labor required to complete a renovation, repair, maintenance, sustainability or new construction project. Overhead & Profit – Temporary facilities, utilities, tools and safety and security costs. How to Estimate Hard Construction Costs.

Colorado Verified Statement of Claims on Public Projects A Colorado Verified Statement of Claim (VSOC) ensures subcontractors and suppliers get paid for labor and/or materials provided to a public construction project. The claim must be signed under oath and only include amounts due for work or materials provided.

Everything starts with cash because "cash is fact, profit is an opinion." Cost of Goods Sold ( Direct and Indirect Costs including Labor, Material, Other and Subcontractors). We take care of your books for you, so you can get back to the job of running your business and generating profits. Job Deposits.

Cost data was truly reflective of local market conditions, by locally researching all construction labor, material, and equipment costs. Additional non-prepriced line items can be easily created from existing UPB line times at a detailed level, include changes to material, labor, crew, and equipment costs.

GENERAL – Cost data is organized using MasterFormat2004+ [1] and includes detailed line item description and associated material, equipment and labor as appropriate. BEST VALUE – As noted, all unit price line item provided incorporate locally research labor, material, and equipment costs.

Each line item has a description in common terms and “plain English” without excessive use of abbrievations, and details breakdowns of material, equipment, and labor costs. Costs should not include contractor overhead and profit, or other items as noted in the JOC. replacement. item will be used. Then the Contractor.

.” Every construction project is a gamble – you’re betting that your estimate is accurate, that labor and material prices don’t go through the roof, etc. Change orders can be harder to manage – and present more of a profitability challenge – than pre-planned project work. Yes, change orders are nearly inevitable. Dexter + Chaney.

Contractors That Do Not Earn Large Profits see contractors bookkeeping services as overhead which leads to the following profit drains: They get a cheap computer, tiny monitor, garbage printer, tiny desk and broken down chair that even the dog would not sit in and tell the bookkeeper this is all the company can afford.

Labor , materials , machinery, transport, overheads and profit). Judging different labour, materials, machinery and money and resource optimization. But if the under following elements are tagged in: Material cost without considering the squanders. But the overhead is normally 3 - 7.5

project task/line item, a full description in plain English, a unit of measure and a corresponding unit price, including labor, material, and equipment details, and an associated approved contractor coefficient are to be the basis for Contractor compensation. coefficient (reference table of allowable overhead). authorization.

We organize all of the trending information in your field so you don't have to. Join 116,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content