This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

1 challenge many contractors face is profit shrinkage or profit margin fade. I often hear company owners say that they bid using a 15-percent markup for overhead and 10 percent for profit. I often hear company owners say that they bid using a 15-percent markup for overhead and 10 percent for profit.

For small business owners like you, understanding this process could be the key to increasing your profitability and ensuring that every job is priced right. Welcome to a world where every material, labor, and overhead cost is meticulously tracked to unveil the actual cost of doing business.

He promoted a charge-out rate 20% below the industry average, explaining that his overheads were lower than those of larger companies. This was how John learned that trading for sales and trading for profit could be different. Chasing sales revenue is fine, provided your prices give you a sustainable profit.

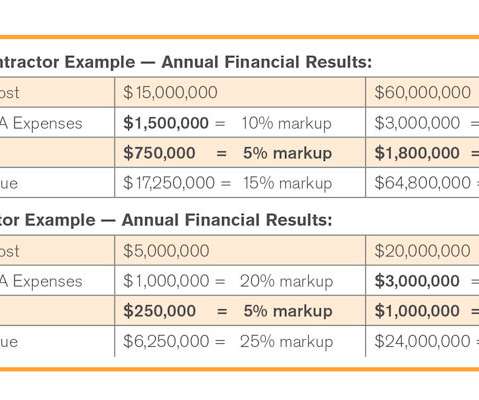

It’s nearly impossible to make any money when contracts allow just 10% and your subcontract only allows for 15% total overhead and profit markup on change orders, or time and material costs plus work. The typical commercial contractor’s annual overhead and profit markup look much like those in Figure 1.

Understanding and managing your gross profit margin is crucial to ensuring the sustainability and profitability of your business as a construction contractor. Profit is the money left in your business after all your expenses have been paid.

People and material make up the lion’s share of a contractor’s overhead, so it’s no surprise that efficiently managing these is the best way for contractors to improve their profitability. 5 Technologies the Modern GC Should Be Using in 2021. Alex Headley. Fri, 05/28/2021 - 07:30.

To build a profitable construction business, owners must be focused on key performance indicators (KPIs) and bottom-line numbers. These KPIs are centered on sales revenue, overhead, profit markup, labor costs per unit of work, and your updated job cost labor for every project. 6 Numbers You Need to Know. Sat, 12/31/2022 - 07:39.

Profit Starts With Knowing Your Numbers ccapoccia Mon, 03/11/2024 - 10:15 The key to building a successful construction business: knowing and managing your numbers. You can’t bid projects right unless you know your job costs, production rates, actual overhead and profit goal.

Imagine your company as a funnel with a shut-off valve controlling the flow of profit output. The funnel absorbs and reduces the profit output by paying invoices for job costs and overhead expenses. The leftover flow is net profit cash exiting the end of the funnel into your equity account.

Understanding COGS isn't just about accountingit's about making smart decisions for profitability, pricing, and more. These include materials, labor hours, and even manufacturing overheads. COGS provides critical insights into your business's efficiency and profitability. What is the Cost of Goods Sold (COGS)?

1 challenge many contractors face is profit shrinkage or profit margin fade. I often hear company owners say that they bid using a 15-percent markup for overhead and 10 percent for profit. I often hear company owners say that they bid using a 15-percent markup for overhead and 10 percent for profit.

After calculating material quantities with your takeoff, estimating adds costs to all facets of the project, from materials and labor to overhead and markup. Waste and overhead can also be added to arrive at the project cost. Estimating is the backbone of a construction project, and it’s essential to get it right to win bids.

The IGCE consists of the anticipated costs to include direct costs (labor, products, equipment, travel, and transportation), indirect costs (burden on labor such as fringe benefits and labor overhead), material overhead, general and administrative (G&A) expenses, and profit. Contractor profit and overhead are NOT included.

Each aspect, such as materials, labor, equipment, and overhead, should be itemized separately. Overhead and Profit: Factor in overhead costs and profit margins using the establish/accepted coefficient. Unit Costs: Assign a unit cost to each line item. This could be the cost per unit of measurement (e.g.,

The coefficient generally must include all project general conditions as described in the contract, including but not limited to supervision, overhead and profit. They select corresponding line items out of the Unit Price Books and compare actual costs including general conditions, overhead and profit.

It should be used to account for contractor overhead and profit. A unit price book should represent the costs for construction tasks (material, labor, and equipment) without contractor overhead and profit. should simply include contractor overhead and profit. Cost Adjustment : A coefficient less than 1.0

General / Prime Contractor Overhead. General / Prime Contractor Profit and risk. Labor (Both during Normal Work Hours and Outside of Normal Work Hours). Materials. Equipment. Subcontractor costs. Subcontractor mark-ups. Payment Bond premium(s) (please note that Payment Bonds are required for task order. projects valued over $35K; 9.

The base rate does not include overhead and profit, however, can be added if needed. Overhead and profit markups are not included in the pricing, but can be added electronically to the database as needed. General overhead and profit can be added by percentage if desired. General Conditions.

You can’t bid projects right unless you know your job costs, production rates, actual overhead and profit goal. How to Set Financial Targets to Achieve Business Goals ccapoccia Fri, 02/09/2024 - 13:22 The key to building a successful construction business: knowing and managing your numbers.

Maybe you started your company with a few friends and relatives as your earliest clients, and you thought your overhead expenses would be low since you worked out of your home. You made a decent living for yourself, hired a few sub-contractors per project, paid your suppliers, and earned a profit—at least that is what your tax preparer said.

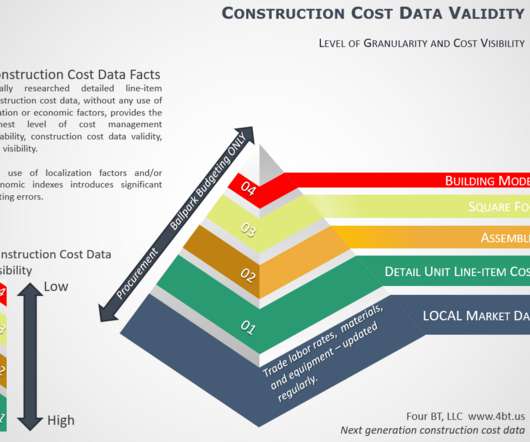

Profit and overheads should be considered separately. To mitigate variables, the unit price cost database should only reflect the direct costs of labor, material, and equipment, fringes, and insurance. for the local market. Cost must be updated regularly.

By Bruce Jervis A wrongfully terminated contractor is entitled to recover lost profit from the project owner. This is the profit the contractor reasonably anticipated had the contractor been allowed to perform the contract; it is a well-recognized element of damages for breach of contract. That was the case recently in California.

A properly-sized commercial general contractor is going to maintain a certain amount of overhead. Commercial construction companies need fees to cover their overhead. By not showing its lowest possible bids, a commercial general contractor may be cherry-picking more profitable bids for itself and its subcontractors.

Briggs & Forrester Group saw pre-tax profit halve to £1.6m The engineering services arm, which is the largest division within the group, has now been streamlined with operations rationalised from four to two regions – South East and Western – to bring significant overhead savings. after suffering a £1.6m

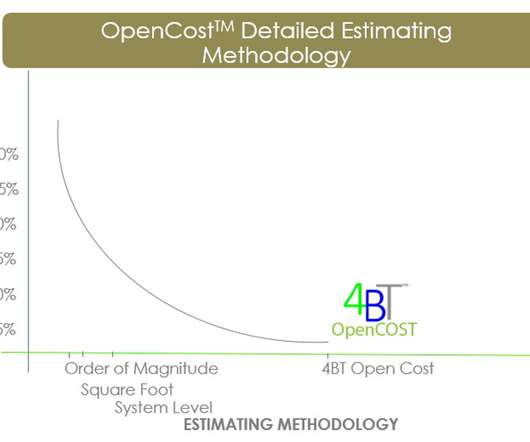

No inclusion of builder/contractor overhead or profit. Specific local market research with zero use of location factoring (city cost indexing) or economic factoring (economic indexes) 3. Organization using expaned CSI Masterformat. Timely updates – Data must be update quaterly at minimum. 4BT updates 1.2+

Are you turning a profit? The most profitable and efficient construction companies have learned to get better results doing more with less. Why sustain a staff with top heavy overhead when using an outsource estimating company can cut annual expenses? Are you losing your market place?

In the construction business, profitability largely depends on keeping overhead down. This applies particularly to construction equipment, the rising costs of which can burn you at both ends when the economy goes south.

With profit margins slimming, a logical way to reduce overhead expenses would be to reduce or eliminate education benefits. What value does that bring to your company? These are common question for construction business owners who are assessing the value of paying for an employee's graduate education.

UPB = Unit Price Book, i.e. 4BT JOC Unit Price Book General Conditions = Indirect Costs OHP = overhead and profit Coefficient = Adjusted UPB + general conditions/OHP % The post JOC Program Workflow appeared first on 4BT. JOC PROGRAM WORKFLOW via 4BT.us – Best value JOC Program solutions.

My guess is that more than 75 percent of all contractors don’t know the right markup to use for overhead and profit. I left shocked at the number of business owners who don’t know how to price their work. They just bid to get the work at whatever the customer will pay.

The disconnect between these entities has created problems in the past, and focusing on these connections enhances collaboration and improves the profitability of construction projects. “ As companies grow, their overhead expenses can also grow.

Here’s a listing of what is typically included in a construction contractor’s Job Order Contract coefficient… Contractor’s overhead and profit. Subcontractors’ overhead and profit. What’s in a JOC Coefficient should be specifically detailed in the Job Order Contract Request for Proposal.

Factors such as profit potential, public demand and downright coolness all led them to answer in the affirmative: meta is coming. . Maybe the metaverse can make it more interactive, enabling people to operate a door or open up a ceiling access hatch and see what’s planned for the overhead space. A means of making money . “If

Example include, general and administrative and other overhead costs, insurance costs, bonding and alternative payment protection costs, protective clothing, equipment rental, and contractor’s profit. Subcontractors’ overhead and profit. All costs associated with bonding (specifically including bond premiums).

The coefficient generally must include all project general conditions as described in the contract, including but not limited to supervision, overhead and profit. For instance, a coefficient of 1.20 would represent a 20% markup. It represents the total cost for an installed unit.

Basically, I not only marked sub costs up a meager 5% for overhead and profit, but I also missed about $10,000 worth of scope (by accident of course). However, there are still projects out there, and companies are getting them – but how?

When used in Job Order Contracts, a unit price historically does not include contractor profit and overhead as this is account within the JOC co-efficient. The post Job Order Contracting – Education & Training Note #201 – What is a unit price appeared first on 4BT.

Reviewing QuickBooks Profit And Loss Reports - From our construction accounting clients reminded me of something I learned in my own construction businesses a long time ago. Change is not always easy but it’s necessary to grow a healthy and profitable construction business.

The reason is that the OpenJOC UPB is locally research and does not include contractor overhead and profit. The contractor’s JOC coefficient includes overhead and profit, thus the unit price book should NOT include overhead and profit.

Coefficient make up defined in contract and examples of items that may be including are overhead, profits, taxes, fringe benefits, permits, clean up. (Specifically for Job Order Contracting, though Integrated Project Delivery is similar and used for major new construction). Owner competency and leadership.

Construction Profits Are Simply. Income - COGS - Expenses] = Profit. "If Let''s Get Some Answers - Contractors and sub-contractors know there is more to profits than what is shown above and most of you rely on your "gut feel" to know when project has made a profit or not. The Short Video Below Shows A Sample Of It.

In it, he discusses one of his core concepts — contractors must price their work with enough mark-up to cover the overhead and operating costs, and allow a reasonable profit. Michael Stone has published an eletter article that should be essential reading for every contractor. appeared first on Construction Marketing Ideas.

We organize all of the trending information in your field so you don't have to. Join 116,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content